In Part 1 we discussed fixing your spending using direct deposit and subsavings accounts to keep your spending constant over time. Let’s continue with the next steps in the blueprint to retire early.

Step #2 – Max out all your tax-advantaged savings & put any extra in a taxable investment account

Now that your spending is fixed, it’s time to sock away the excess cash in tax-advantaged investments. If you want to save more cash than you are today, take a hard look at your spending and cut what you don’t care about with my savings tips. (Three separate links. Count ’em!)

If you have any high-interest debt, which generally means credit card debt, pay that off first. It makes absolutely no sense to pay a guaranteed 12% to Wall Street fat cats while trying to earn a very volatile ~8% in the stock market (or a guaranteed 4% in a bank account.) Paying off high-interest debt is the best investment you can make. One exception to this: if your employer offers any 401k matching contributions, contribute the minimum to get all of that first, and then focus on paying down your credit card debt.

Your mortgage should be cheap today, so just pay that off at a normal 30-year fixed rate mortgage pace. With good credit you should have a ~4% or lower interest rate, if not, refinance.

For student debt or a car loan, if the interest rate is higher than 7-8%, you might consider paying that off before contributing more to retirement accounts. Some of you might be planning on getting your student loans forgiven after 10 years if you pay only the minimum, which means it’s in your best interest not to pay off the debt more quickly. Sit down with a clever financial friend who’s good with Excel and ask them what makes the most sense.

If your employer offers a 401k/403b account, max that out ($23,500 per year in 2025.) If you can contribute to a Roth IRA, max that out next. (If you’re in the lowest two or three tax brackets, reverse the order: max the Roth IRA out first, then contribute more to your 401k, but remember to always get any employer matching first no matter what your tax situation.)

The reason tax-advantaged savings are so important is because giving extra money to the guv’ment when you don’t have to is a huge drain on your savings. If you’re in the 24% tax bracket, what would be $0.76 in your savings account becomes $1 in your 401k. This is an instant, guaranteed 31.5% return on your money (1.315 = 1 / 0.76). There is no better deal out there. (The math on the Roth IRA is exactly the same, except in reverse: you pay income taxes now, but don’t pay them in retirement.) If your employer matches your contributions dollar for dollar, that’s a 100% + 31.5% = 131.5% instant, guaranteed return on your money.

You get tax-free growth as well

Tax-advantaged accounts like IRAs and 401ks, and HSAs for that matter, grow tax-free as well. Normal, taxable investment accounts make you pay taxes every single year on any dividends generated, and also whenever you sell stocks that have increased in value (‘capital gains’.) This is also a huge drag on your money.

If you started with $10,000 in a taxable account and $10,000 in a tax-advantaged account like an IRA or 401k, after 20 years you would have gained $30,000 in the taxable account at 8% annual returns. We’ll assume 3% of that was in dividends. Even if you’d never sold a share and thus paid zero capital gains, your 24% tax rate on that 3% in dividends would have cost you $6,600 dollars in growth. That’s the difference between the $36,600 you would have gained in the retirement account (which is 19% more money!)

Lastly, if your employer offers a Health Savings Account (HSA) health insurance option, and it makes sense for you to choose that insurance, max that out as well. Keep in mind that any employer contributions to your HSA reduce the amount you can contribute, and that you can contribute twice as much if your family is also covered under your plan. (I use my HSA funds to pay for out of pocket health care expenses for me and my family because the earnings come tax-free when you do that. Having these HSA funds available will really help when I retire early and have to get by with high-deductible health insurance.)

If you’re saving for your child’s college (or even K-12 private school), invest in a 529 plan to receive tax-free growth + tax-free earnings if you spend the money on qualified education expenses. For non-education expenses for your child, consider a Uniform Transfer to Minors (UTMA) account, but keep the earnings on it under the IRS-approved tax-free figure ($1,050 per year in capital gains + dividends as of 2020.)

After you’ve done all you can on the tax-advantaged front, put any extra into a plain ol’ taxable investment account. I recommend keeping all your accounts under one roof as much as you can for easier management. I prefer and recommend Vanguard, but Fidelity is fine too.

Now we see the entire Early Retiree picture:

Step #3 – Invest long-term in stock index funds with low fees & minimal taxes

Now that you’re saving like a bo$$, you need that money to grow as rapidly as possibly without taking on any significant risk of permanent loss of capital. This means you should put all your long-term savings into a diversified, low-fee index fund like the Vanguard Target Retirement Fund (the easiest and slightly more conservative option since it’s 90% stocks 10% bonds and rebalances automatically), or go 100% stocks and split it up 70-30 between the Vanguard Total Stock Market Index and the Vanguard Total International Fund. More on choosing investments here.

Mr. Market

You don’t, and shouldn’t, care about periodic stock market ups and downs, because you’re socking that money away for at least 10 – 30 years from now, and you’ll be spending it over an even longer period of time, leaving most of it to keep growing well into your retirement. As long as you don’t get laid-off, recessions are great for juicing your stock market returns because you get to buy a lot more shares of stock than you would at higher prices.

Don’t try to time the market, and don’t buy more when the market goes up or sell when it goes down. That’s some roody-poo candy-ass foolishness that Early Retirees don’t fall for. Just continue to steadily invest your excess savings from your direct-deposited cash as it fills up in your savings account each pay period. (This is known as ‘dollar-cost averaging’ because you end up buying at the average market price over time, which minimizes your risk of getting a return that’s particularly higher or lower than what the market returns over time.)

Feel free to automate this investment if it makes it easier for you. I just wait until my savings account has a few thousand bucks in it, and then I manually ship it on over to my investment account at Vanguard using their app or website. Make sure to do this periodically and don’t be one of those money-left-on-the-table suckers with thousands earning next to nothing in a bank account instead of compounding it exponentially in stocks like your name was Warren Buffett.

Very important warning: aggressive savers planning for financial independence know that there are no ‘short cuts’ to wealth. Investing in something you don’t understand is a great way to go broke. (And you always THINK you understand it before it’s too late.) Bad ideas for most people include real estate (high-fees, scary leverage, lots of knowledge required, terrible diversification), currency (‘FX/Forex’), crypto (ex: Bitcoin) and any kind of ‘day-trading’, low-quality “junk” bonds sporting illusory high yields, and that business scheme that your frat buddy dreamed up. Another bad idea is picking individual stocks, or non-indexed, high-fee mutual funds, both of which doom foolish investors to underperformance. If you must speculate by taking on a few risky investments that you think are good ideas, do your homework, educate yourself, and limit these speculations to no more than 10% of your portfolio.

Instead of chasing get-rich-quicker ideas, smart savers and early retirees will cut fees and taxes to the bone and take the exponential long-run returns of the stock market year after year after year. Index stock fund investing is not only the higher-return option, it’s way easier and cheaper than any other form of investing, allowing you to set your investments practically on auto-pilot while you spend more time enjoying life vs worrying about the market or that lousy penny stock your brother-in-law said was a sure thing.

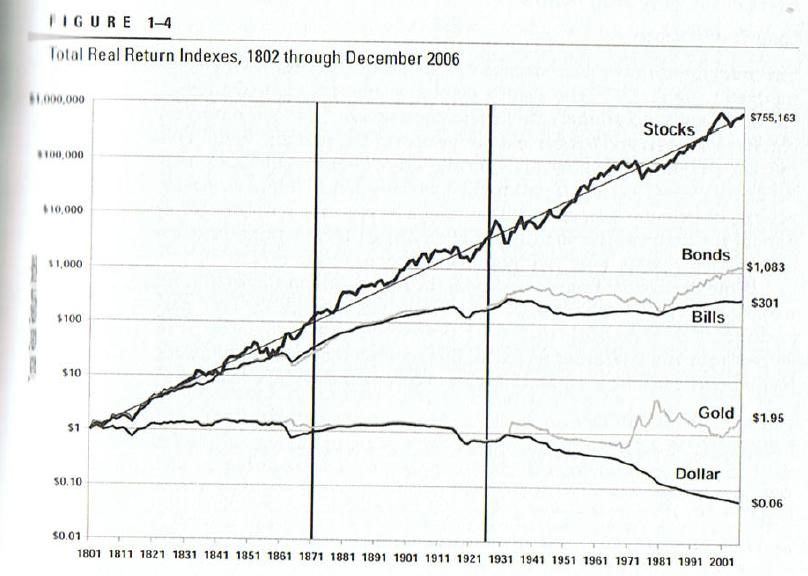

Source: The above log-chart showing the astronomical returns of stocks vs all other asset classes is from Jeremy Siegel’s excellent Stocks for the Long-run

The only financial short cuts you’ll find are downward ones to poverty. For every person who got lucky doing something stupid (that they will advertise as brilliance), there are ten other ones who went quietly broke that you never hear from. So, ignore get-rich-quick scheme peddlers, brokers, “advisors” that are brokers in disguise, financial salespeople who are sometimes brokers, but might be insurance or real-estate agents, and financial story-tellers.

Your savings rate is the only thing that matters

Your savings rate is the only thing that matters↗

Instead of go-broke-quick schemes, do what I’ve described above and focus on increasing your savings rate: the percentage of your take-home pay that you invest.

If you had ZERO savings in the bank right now, investing 50% of your take-home pay starting now means you can retire in 16 years. If you began saving 2/3s of that pay, you’d be able to retire in just 10 years. That’s right, if you’re 30 and haven’t saved a dime up until now, a dramatic change in your savings rate could have you retiring by 40 – 46. And that’s with ZERO savings now; it’s even faster if you already have some savings.

It’s deliberate, and even straight-forward if you use the tools I recommend: set up your saving & expenses infrastructure and start maxing out your tax-advantaged accounts in the right investments.

Conclusion

Increasing your savings rate isn’t magic. Fixing your spending (Part 1) so that you can invest ever-increasing amounts of money in low-fee stock index funds inside of tax-advantaged accounts is the bedrock of any legitimate financial independence plan.

On the earnings side, increase your income over time by asking for raises, getting promoted, and shifting positions and companies to more lucrative jobs over time.

Feel free to stop reading here and start implementing the plan above using the links provided!

If you want to get into the weeds a bit, there are some more details to consider below and in the next article (which you could always come back to later. These posts aren’t going anywhere!)

Now that you know what steps to take to retire early, find out how much money you need at your specific retirement age.

Optional tweaks to the blueprint

If you are motivated to make more money by allowing yourself some extra consumption when you get a raise or a bonus at work, or work more hours, feel free to fix your spending as a percentage of your income instead of a fixed dollar amount. One of my financial heroes Ramit Sethi recommends that approach.

That said, I find that a fixed dollar amount is much easier to set up and manage. There’s often no ‘percentage of income’ option in direct deposit set ups, and no automatic percentage transfers between accounts. I find that automation is absolutely essential to making this work, so fixed dollar might be your only option. You could instead manually give yourself some motivating chunk (10 – 25%, say) of any extra income you generate through your hard work or hustle, and keep the rest of your spending fixed.

Fixed dollar budgets also build in some spending discipline that I enjoy, but I’m also a huge weirdo that loves spreadsheets and thinks that financial planning is not actually a chore but a fun game invented by Benjamin Franklin as proof that he loves us and wants us to be happy.

What about the self-employed or others that might not have a steady income, let alone direct deposit?

Instead, you can dump everything in your savings account via direct deposit/business income, and then create a fixed monthly automatic transfer from your savings into your checking that equals your spending needs. I describe this method here.

Try to fix your expenses to the lowest monthly amount of income you think you’ll have coming in so that any extra becomes long-term savings.