This is the second post in our series of steps you can take in 15 minutes or less to make a huge improvement in your finances. In step one, we talked about the importance of boosting your 401k contributions, even if only by 2-3%.

Now we’re going to use a simple trick to save effortlessly and never worry about over-spending again.

TL;DR – Send all of your income into a Savings account instead of a checking account. Then set up a recurring monthly transfer from that Savings account into your checking account at the end of each month to cover your average expenses. This effectively ‘fixes’ your spending at a constant dollar amount. ***This is the best thing you can do for yourself financially!***

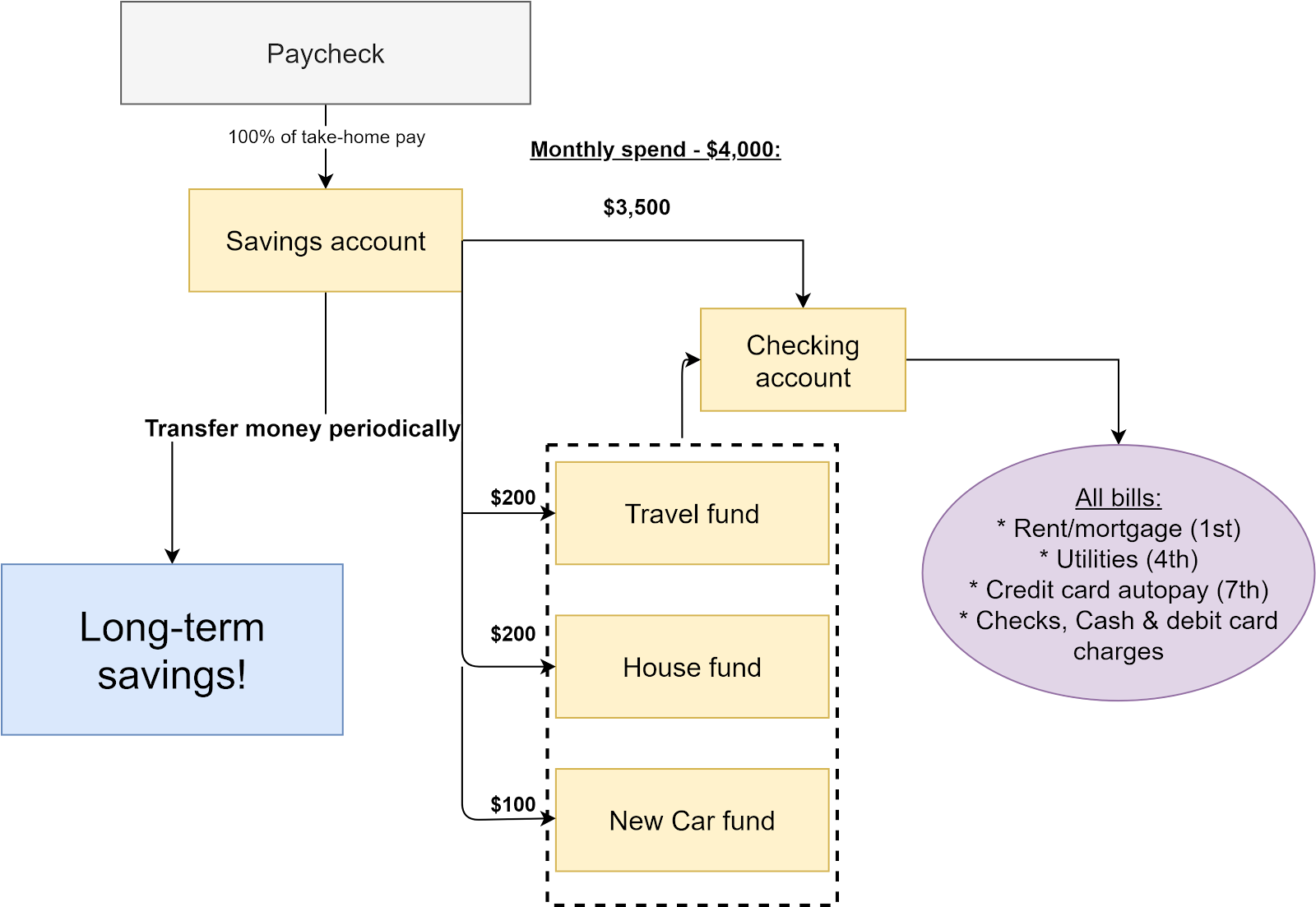

Above: the simplest fixed spending set up, with all spending money going to checking.

- In your direct deposit, or however you get paid, change the banking info from everything going into your checking to everything into your savings account.

- Next, log into your bank account and set up a monthly, recurring transfer from the Savings account that’s getting all your income now, into your checking account that pays all your bills.

- Set the monthly transfer to your average monthly spending (see below for how to get this), plus a little bit extra to make sure you have enough.

- If you can’t be bothered to estimate your spending, just set the monthly transfer equal to your monthly pay. If you get paid monthly, use your last month’s takehome pay stub as your monthly transfer (make sure to use the take-home amount, not the gross!) Get paid every two weeks? Multiply your last stub by 26/12. Twice a month? Multiply your pay by two.

- Optional, but highly recommended: for cars, vacations, weddings, college, and other big, irregular purchases that you need to save up for, either use some of the money that lands in your checking, or (much better) add more monthly transfer to additional savings accounts and send a fixed amount of money to them from your main Savings account. (Schedule these transfers a day after your checking transfer so that the spending money gets top priority in case there’s not enough in your main Savings.)

Above: the complete picture, with extra spending buckets added in.

This simple direct deposit + monthly transfer setup ‘fixes’ your spending so that you aren’t tempted to spend your whole income. This amps up your savings, especially as you get raises and bonuses. It also accounts for irregular income like that of self-employed folks, or those who rely on commissions, bonuses, or RSUs/stock options. It even works for retirees: just set all your pensions, dividend payments, social security, and any other income to go to Savings, and use the monthly checking transfer as described.

Ready to do this yourself in 15 minutes? Follow along below!

Use direct deposit to master your spending and amp up your savings automatically

My employer uses ‘Workday’ to manage employee pay. I clicked ‘Payment Elections’ to get to my direct deposit. Search your employer pay site for ‘payment elections’ or ‘direct deposit’, or ask your HR person how to change your direct deposit if you can’t figure it out.

Here’s what your set up might look like today, with the ‘balance’ of your paycheck all going to checking:

Adjust your direct deposit to send everything to Savings instead

Swap out your checking account number for your savings number in your direct deposit. Get the routing and account number for your Savings account by logging into your bank online.

The Pro’s direct deposit: everything going to Savings, with a monthly transfer to checking (we’ll show that next), and the rest that’s left in Savings to pay off debt, invest for the long-run, or buy a home, and NOT for spending!

Estimate your monthly spending: easy method

If you’re feeling lazy, or spend roughly everything and can’t be bothered to cut back yet, just find your last pay stub, convert it to a monthly amount of take-home pay, round down a little just in case, and set your monthly checking transfer equal to that. If you get paid monthly, use that amount. If biweekly– every two weeks– multiply your last pay stub by 26/12 and use that as your monthly transfer number (or multiply by two so you’ll save two paychecks per year!) For semi-monthly– twice a month–, just double your pay stub. Make sure you’re using the take-home pay amount to compute your monthly transfer, and not the gross!

Think of this as the ‘save tomorrow’ method. Yes, that means everything today will go to checking and nothing will stay in savings. But, when you get a raise or bonus, it’ll get banked in your Savings without you having to lift a finger. The default will be that you save more, and good financial defaults make all the difference.

To start saving some portion of your income today, roughly estimate what you spend each month, erring on the high side. First, add up any large, constant bills like rent or your mortgage that come straight out of your checking account.

Estimate your monthly spending: precise method

Next, average together your last year’s worth of credit card bill and any other bills that come straight out of your checking account (or wherever else you pay bills from.) Include any cash that you took out of an ATM.

For credit cards, log into your credit card(s) online, download the past year’s worth of transactions as a CSV file, and add them up in Google Sheets or Excel and divide by 12. Or, just look at your payments IF you pay your bill in full each month, and add up the last 12 of those and then divide by 12. Many credit card providers also give you annual summaries in January (look under ‘Statements’), so you can just grab your most recent one of those, get the total, and divide that by 12.

Here’s mine from my Chase credit card, which shows $16,035 in 2020 spending (bottom right), which is $16 K / 12 = $1,333 per month. They also give you a useful breakout to understand your biggest spending categories, but we’re not worried about that here.

For bills paid from your checking account, log into your account and do the same thing you did with your credit card transactions. Look for something like ‘Download Transactions’. Make sure to filter out stuff that’s not actually an expense, like transfers between accounts.

I downloaded my checking transactions for the past year into Excel and scanned it quickly for bills. I just had my mortgage, a utility bill, and a handful of checks since I put as much as I can on my credit cards. I added up the bills and checks and divide by 12.

So, let’s say my mortgage is $2,500, my credit card spending was $1,333, and the remaining misc bills that came out of my checking averages $167. That’s a total of $4,000 per month. I also use $200 / month for cash spending, so that’s $4,200. Round up to be safe, so call it $4,500.

Set up the monthly transfer to checking to pay your bills

Now that you have your estimated spending as a monthly number, log into your bank account and set up the automatic monthly transfer at the end of each month to go to your checking. Schedule a few business days earlier if you’re transferring from Savings at one bank to checking at a different bank since it could take 2-3 business days.

Here’s how my transfer looked:

Pro tip: If your rent/mortgage is paid on the 1st, change all of your credit card due dates to be on the 3rd or 4th so that these essential bills get paid soon after you transfer your spending money to checking. Do the same with your utility accounts that come out of your checking if any and if possible. This way, all your important bills are paid soon after you get your spending money, and what’s left over you can spend via a debit card or with cash withdrawals guilt-free since you know you’ve already taken care of your monthly must-pays.

Important: Make sure you have a cash cushion in your Savings account to start the full monthly checking transfer. You could also pad your checking a little bit in the beginning in case you underestimated your expenses. (But, going forward, only adjust your monthly transfer to checking! You want to get in the habit of knowing and sticking to exactly one fixed average monthly spending transfer.)

Set up free overdraft transfers from Savings

Some banks– including Ally Bank, my recommended bank— as well as BECU– over free overdraft protection that works like this: you link your checking account to the savings account that is receiving all your income, and by doing so, your bank will auto-transfer money from savings to your checking to cover any overages that happen in the future.

Ally calls this Overdraft Transfer Service. Make sure to pick the right one since banks often offer their expensive option along with the free one! If your bank doesn’t offer this, consider switching banks.

For Ally, here are the situations in which overdraft does and does NOT kick in:

Consider a spending bucket for ATM cash or debit card purchases

If you use cash for something, consider having a designated checking account that receives a fixed amount per month (from your ‘main’ checking) that you intend to use for cash (or debit card) purchases. I use and recommend Schwab’s free Investor Checking because it reimburses me for ATM fees globally. It’s great for travelling internationally for this reason.

Having a checking–instead of savings– account as a separate spending bucket from your main checking is also great for repeat small-ish purchases that would be a pain to remember to transfer amounts from a savings back to your main checking each time you spend in that category. If you want to fix your eating/drinking out spending, a separate checking account with a debit card to use is the easy way to go.

Splitting your income automatically to spending & saving is the key to getting rich

That’s it, you did it! If you didn’t follow along, take 15 minutes now to log into your company’s direct deposit to dump everything to savings, and then to your online banking to set up the monthly checking transfer. You can always choose your paycheck amount (the ‘save tomorrow’) method to transfer for now, and go back later to update the amount after you’ve crunched the spending averages. The key is to take action and do some form of this right now!

Once you do this, you’ll never have to worry again about budgeting under normal circumstances.

Later, invest your excess Savings

The last step, which you can do a few months later after you’re system has been running, is to periodically transfer the excess money left in your Savings account to invest it. You could set yourself a quarterly calendar reminder to make this transfer, or set up some automatic transfer.

Let me know in the comments if you implement this system, or if you have any other suggestions for making this system, or a different one, work!

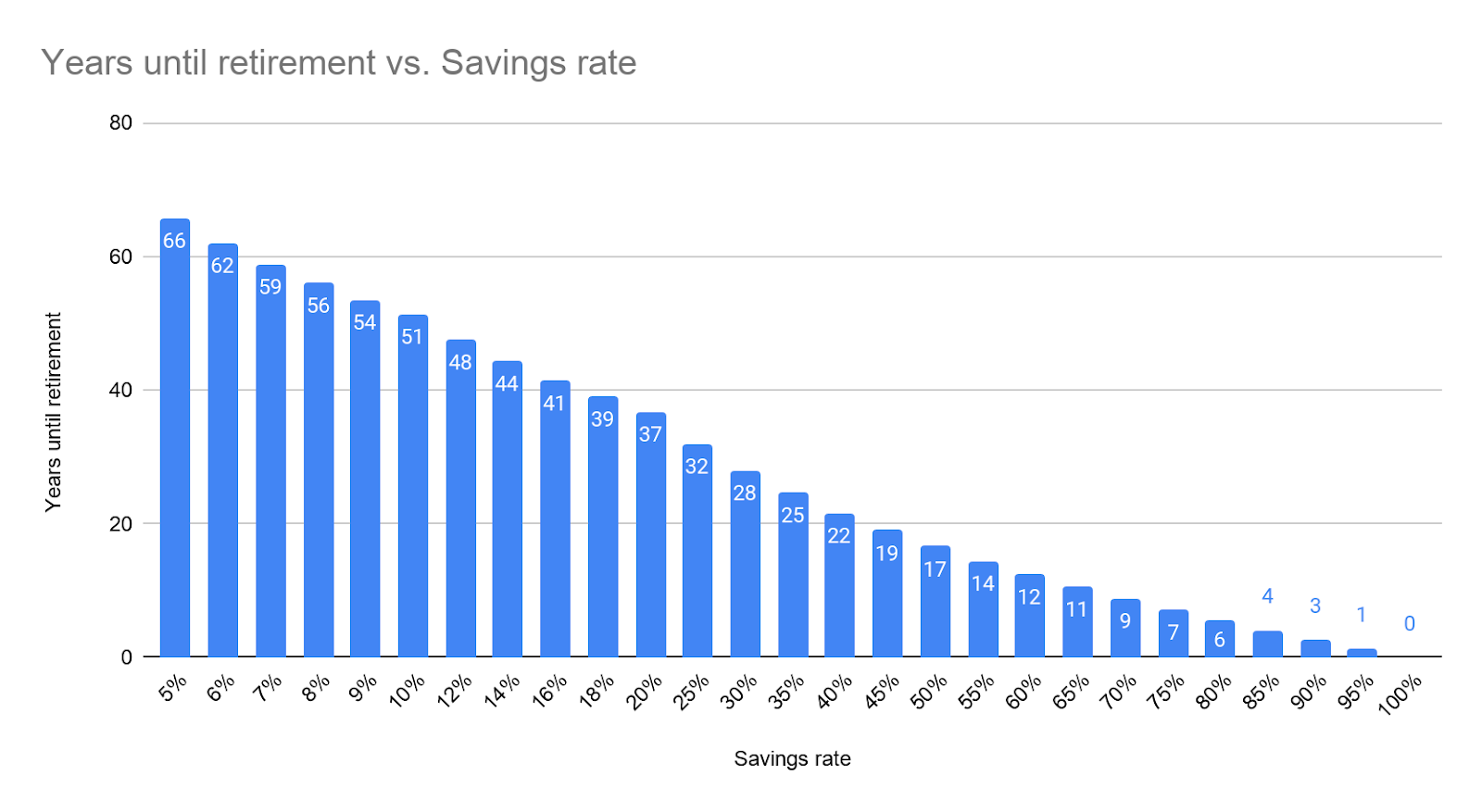

Addendum: your savings rate = financial independence timeline

As Mr. Money Mustache famously pointed out, the only thing that matters to when you can retire/achieve financial independence is your rate of savings (the percentage of your income that you save vs spend.)

The below graph shows how long it would take (y-axis) for someone with no savings or other sources of future income to retire forever* as a function of their savings rate.

*It assumes a 5% real return on investment, which is in line with stock market expectations and history, as well as a 4% withdrawal rate in retirement. I.e.: it’s the time it takes to build 25x your spending with an assumed 5% real interest rate from your investments.