[The exit tax involves] taxing the unrealized gains on [the person giving up their US personhood’s] worldwide assets as if they were sold for fair market value the day before they left.

Essentially, the IRS acts as if you sold all your property (houses, stocks, businesses) the day before you renounce citizenship, even if you didn’t actually sell anything. You are then taxed on the profit that those assets have built up over time.

[..] The U.S. State Department has reduced the renunciation fee to $450, effective April 13, 2026.

Per the article above, if you have less than $2 M in net assets (after subtracting debts), have remained 100% compliant on your US tax filing, AND have averaged less then ~$200,000 in actual annual tax payments (NOT income!) to the US for the past 5 years, you are NOT a ‘Covered Expatriate’, and do not have to pay any exit tax.

For most people working in a country with a US tax treaty who have continued to file in the US, they therefore would only get hit with the US exit tax if their net worth is over $2,000,000 when they renounce their citizenship/green card.

For Green Card holders, “[y]ou are only subject to these tests if you are considered a Long-Term Resident. This means you held your Green Card for at least part of 8 out of the last 15 tax years. If you leave in year seven, you can often avoid the exit tax entirely, regardless of your wealth.”

Exit Tax Exclusion amount

Even if you DO qualify for the Exit Tax, the IRS lets you exclude gains of $910,000 (for 2026), so you still might not pay anything, depending on your unrealized gains when you renounce.

Specified Tax-Deferred Accounts (IRAs and HSAs)

“If you are a “covered expatriate,” certain accounts are treated as if they were fully cashed out the day before you left. This is called deemed distribution.

Which accounts are affected?

Traditional IRAs, Roth IRAs, Health Savings Accounts (HSAs), and 529 College Savings Plans.

The Tax Hit: You must report the entire balance of these accounts as ordinary income on your final U.S. tax return.

The Downside: You cannot apply the $910,000 exclusion to these accounts. They are taxed from the very first dollar.

The Silver Lining: The IRS generally waives the 10% early withdrawal penalty for these deemed distributions, even if you are under age 59½.”

The price at which you have the option– but not the obligation– to buy the stock at. If this price is BELOW the current fair market price at which you could sell the stock for, your options are ‘in the money’. If the current value is BELOW your strike price, you are ‘out of the money’, and the only value in your stock options is the ‘time value’, the chance that the future price will be higher than your exercise price. If the market value never exceeds your strike price, your options will ‘expire’ worthlessly at the expiration date, which is typically around the time your terminate with your employer OR 10 years from when the options were granted to you (NOT from the later date when the vested.) Companies that have not IPO’d or otherwise sold themselves will often adjust the expiration dates so that long-time employees don’t get screwed out of their options at the 10 year mark.

Calculating the value of stock options

The value (market price) of options have two components: the money value, and the time value. Added together, these = what someone would pay for your options.

Money value

The difference between the current stock price and your strike (exercise) price.

Time value

An option has time value because you can’t lose money when the underlying asset dips below the strike price AND the fact that the underlying asset can still increase in value before your option expires. To compute the time value, use this calculator: https://www.cboe.com/education/tools/options-calculator/

Employee Stock Options: ISOs and NSOs

Incentive Stock Options (ISOs) provide favorable tax treatment if you follow some of the rules. If you hold the resultant shares for 2 years after the option grant date AND 1 year after you exercise the options, then you pay long-term capital gains taxes on the different between the market value at sale (sale price) and the original strike price. If you fail to do this, you must pay regular income taxes on the difference between the purchase price of the stock (the fair market value at exercise) and the exercise price.

NSOs can often be held longer past an employee’s termination date with a company, but have less favorable tax treatment. The tax is essentially the same as a “disqualifying disposition” for ISOs.

If consolidating, choose the ‘let my loan servicer pick my repayment plan’ option to get the lowest payment out of the four Federal student loan repayment programs. Your interest rate for direct Federal loans will just be the weighted average of your existing loans, which makes sense. Consolidating also ends your grace periods, FYI, so make sure that’s not a problem for you.

If your loans are all Federal, you’ll still get the same ‘credit’ towards PSLF (Public Service Loan Forgiveness, the 10 year– 120 months of payments made– debt forgiveness you get for working for a non-profit or government entity. Because, ya know, you can’t work for the public good at a for-profit institution where people engage in voluntary transactions for their mutual benefit…)

Your strategy for student loans should be to (1) get the lowest payment (and effective interest rate) possible then (2) pay the minimum due and hope for them to get forgiven either under PSLF or some future Democratic policy. Or if your rates are actually pretty high (say, > 6-7%, and this is calculating the true rate AFTER the IDR payment is reducing your standard repayment), paying them off (God forbid you should be expected to do that!)

Parent Plus Loans

Direct PLUS Loans for Parents are loans where the parent of the student takes on the debt, not the student. The rate is fixed for the life of the loan, and you must also pay a fee as a % of the loan (4.228% as of writing for loans disbursed after 2020) that comes out of the balance you receive.

Parent PLUS Loans have the following repayment term options:

Standard Repayment Plan: Under the Standard Repayment Plan, the borrower makes fixed monthly payments for up to 10 years.

Graduated Repayment Plan: Under the Graduated Repayment Plan, the parent makes payments for as many as 10 years. However, the plan starts with lower monthly payments that increase every two years.

Extended Repayment Plan: The Extended Repayment Plan allows borrowers to repay their loans over an extended period of as much as 25 years.

You can defer repayment until after the student graduates, but the interest still accumulates. Parent PLUS Loans are eligible for forgiveness under Public Service Loan Forgiveness (PSLF) and the Income-Contingent Repayment plan.

Parents have many options to repay their PLUS Loans and can even change their repayment program over time. Here are some of the different ways parents can choose to pay off their federal debt:

Income-Contingent Repayment: Parents can gain access to the Income-Contingent Repayment plan if they consolidate their federal student loan debt. It caps payments at the lesser of 20% of your discretionary income divided by 12 or the amount you’d pay in fixed monthly payments on a 12-year repayment plan, adjusted based on income.”

“One workaround for the fixed payments and ineligibility for loan forgiveness is to use a Direct Consolidated loan. That requires rolling the Direct PLUS loan into a new, bigger loan — possibly with a higher interest rate.

That loan would be eligible for income-contingent repayments and could be forgiven after 25 years of payments. Parents who qualify under the Public Service Loan Forgiveness program will be able to apply after 10 years of payments.”

“Income-contingent repayment plans: Monthly payments are capped at 20% of your discretionary income. After 25 years of on-time payments, the balance is forgiven. This can be a good option if you’re approaching retirement since many retirees have limited income. Your payments could be $0 in some circumstances. You’ll need to consolidate your loans to qualify for this option.

Extended repayment plan: The standard repayment term for federal student loans is 10 years, but an extended repayment plan stretches the repayment period to 25 years. Of course, the longer repayment term causes you to pay more interest.”

Married Filing Separately trick for married couples to reduce your IDR payments

If you have the student loan debt AND you make significantly less than your spouse AND you do NOT live in a community property state (like Washington, Wisconsin, and California; this is because your income will just be half your total income as a couple), you might be able to significantly reduce your student loan payment under an IDR like IBR or RAP. If you are on a Public Service Loan Forgiveness (PSLF), artificially lowering what you have to pay might result in far higher forgiveness later.

Compute the savings on student loans vs any extra taxes you will pay/cost of tax benefits you will miss out on from switching from Married Filing Jointly to Married Filing Separately (MFS). Use your tax software or ask your accountant to model your taxes under each scheme to compute the difference on the tax front.

Calculate any extra taxes you’ll pay vs filing jointly

Lost Deductions & Credits: You lose eligibility for benefits like the student loan interest deduction, adoption credits, and certain education credits.

Higher Tax Brackets: The MFS tax brackets are less favorable than Married Filing Jointly (MFJ), meaning your combined household tax bill will likely increase.

Retirement Limitations: The income phase-out limits for contributing directly to a Roth IRA drop to almost zero when filing separately.

Filing an extension to delay IDR increases when your income goes up

Another trick, as described here, is to file an extension on your taxes in the tax year that your income went up so that your prior year income is used when it comes time to recertify your income for FAFSA’s IDR repayment plan.

From that article:

“Consider a physician with $300,000 in student loans at 6.5% interest. They’re pursuing Public Service Loan Forgiveness (PSLF) and filing taxes separately from their spouse to keep payments based on their income alone.

Their 2024 tax return reflects residency income of $80,000. On the Income-Based Repayment (IBR) Plan, that works out to roughly $400 per month. But this year, they transitioned to attending, earning a blended income of about $165,000 for 2025 — moving to $250,000 in full-year attending salary by 2026.

That’s a difference of over $700 per month (more than $8,400 per year) just by strategically extending your tax filing deadline. If you’re pursuing PSLF, that’s $8,400 more that gets forgiven rather than you paying it out of pocket.

The system only links to what’s been officially filed. When extensions are used consistently year over year, your payment stays approximately 12 to 18 months behind your actual current income.”

This strategy only works if your annual IDR recertification date falls between April 15 and October 15.

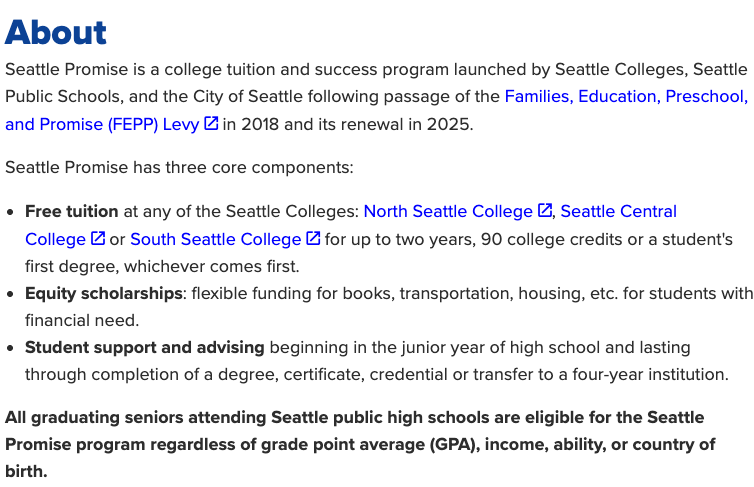

If your kids go to a Seattle public high school, they can attend one of the Seattle Colleges tuition-free for the first two years of school.

Tuition & fees for years 3 and 4– if continuing on for a Bachelor’s and not stopping at an Associate’s degree– are roughly $27,000/year* as of 2026. There are other Seattle Colleges scholarships too.

Seattle Promise is the program that sponsors this via a tax levy that run for 6 years starting in June 2026 (so expiring unless voters renew in June 2032.) Read more about it here.

The Washington College Grant— something you are automatically considered for when completely FAFSA (or WAFSA for those without legal US residence status like ‘Dreamers’ or undocumented immigrants)– is another option for Washington state residents outside of Seattle.

*Data as of June 2026. Three 15 credit quarters is a full year, so multiply the below by three to get annual tuition & fees:

Student Residency Status

Annual Tuition (15 credits/quarter)

Approximate Mandatory Fees

Total Expected Annual Cost

WA State Resident

$8,131.35

$663

$8,794.35

Non-Resident (U.S. Citizen)

$8,729.10

$663

$9,392.10

International Student

$22,487.40

$663

$23,150.40

Screenshot of the programs’ description. The same link has a list of eligible Seattle high schools: