The best long-term evidence for the superior returns of stocks— i.e.: investing in businesses– that I’ve come across is Jeremy Seigel’s excellent book Stocks for the Long-Run. While I remain firmly convinced of the likely outperformance (net of taxes & fees) and low risks of permanent loss of capital of publicly-traded stocks (purchased via low-fee index funds) relative to other asset classes, it’s good to periodically check one’s assumptions against data.

To that end, here’s a smattering of information that to me, helps continue to make the case that stocks, especially US equities, are likely to continue to be the best thing for investors of all wealth & income brackets to invest the bulk of their fortunes in.

From Blackrock, here’s returns from the past 10 years for many asset classes, including the annualized returns at the far-right:

You can see from the far-right column above that US equities crushed all other classes, with other developed markets (Japan & EU) not far behind. I’ll give a nod to REITs as well, which are what I recommend for clients who really want a real estate-only component of their portfolio as a way of owning real estate without the headache, illiquidity, fees, taxes, and lack of diversification inherent in owning individual properties. (That said, your own home can be a fine investment, considering various subsidies and tax-advantages.)

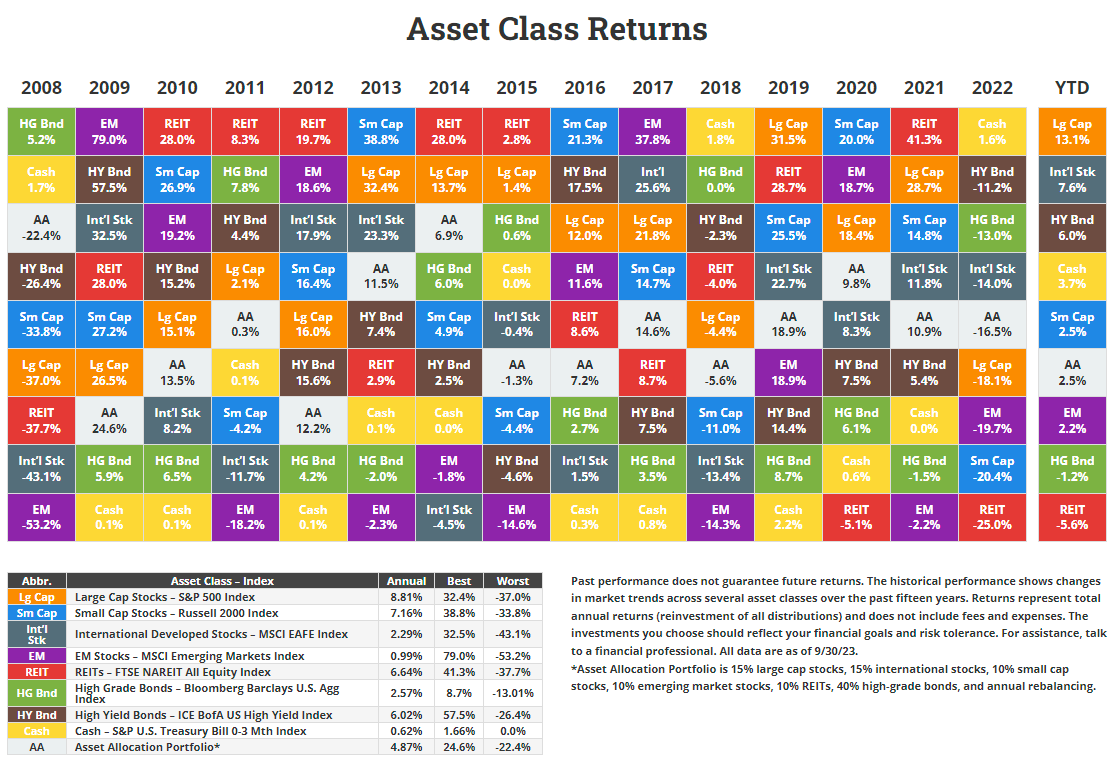

Here’s a similar chart from another source going back to 2008:

Source: NovelInvestor.com

Source: NovelInvestor.com

Again, US stocks were at the top, followed by REITs, bonds, then international stocks.

What NOT to buy for the long-run?

Commodities, gold, cryptocurrency, and vacant land

Any asset that doesn’t do anything is a bad candidate for long-term growth. Why? It’s not productive. Owning ‘commodities’– coffee, sugar, oil, pork bellies, gold– can only earn you positive returns above inflation if you get lucky enough to hold them in an inflationary environment. Otherwise, stuff will just increase in value with inflation on average, because unlike a business or a piece of productive real estate (farm, rental or commercial property), a lump of gold or a barrel of oil doesn’t create anything more of itself over time. Ditto for cryptocurrencies. All of these assets are purely speculative plays. If you yourself are an expert in the valuation of these products, sure, you might have an edge, but considering how many well-funded ‘experts’ on Wall Street and around the world are playing this game against you, I wouldn’t bet on your chances.

Vacant land that you fail to develop or monetize as a rental or commercial or farming property falls into this category as well. You should be vacation property because you intend to enjoy it relative to the costs of other leisure rentals or activities, not because you intend for it to make you rich.

Art, wine, vintage car collecting could all go into this category as well unless you are truly an expert in spotting deals AND are ruthless in re-selling for the highest prices. As with any venture where you think you can ‘beat the market’, compare your returns over a long period of time making sure to value your time and including any taxes, fees, etc to reduce your returns by.

Cash value life insurance, annuities, and rental real estate

Assets that are either too risky or too time-consuming also get crossed off my list. The former include anything hard to evaluate or that include high fees. Cash value life insurance and annuities almost always have egregious fees and the supposed ‘tax advantages’ are largely illusory; plain stock index funds in a brokerage are very tax-efficient if you buy and hold index funds for the long run. Individual real estate holdings like a rental property fall into the latter category of ‘too time-consuming/hard’ for most investors. Read any of John T. Reed’s excellent books on how to manage property for profit, and then come back and tell me it sounds like a walk in the park to you.

Non-publicly traded businesses: hedge funds/private equity, angel investing

Theoretically, if public stock investing is great, so might investing in non-publicly-traded equity. In practice, it either requires a lot of ‘deals’ to achieve sufficient diversification, there’s problems with liquidity (no market to trade your shares on), and a lot of ‘angel’ investments are just that: angelic because they expect NOT to earn anything on their investment in most cases, and they’re usually right!

I personally have made two angel investments in my life, knowing full well it was largely speculation for a good cause or people I wanted to support, and both turned out terribly from a financial perspective. I was ok with that potential at the outset, and these weren’t dollar amounts that mattered much relative to the sums I have in low-fee index funds.

Various hedge fund/private equity ‘opportunities’ may come your way with high minimum investment amounts, and they suffer from the same high-fee & specific risk problems that publicly-traded mutual funds suffer from: you could lose your shirt if they guy you’re paying makes some dumb bets, and even if he does ok, his fees will likely eat up any gains relative to the overall market that you would’ve made. There are also liquidity problems here too since small money managers want their clients to lock up the funds for long periods of time since they don’t want to have to liquidate their fund’s positions at a bad time.

Cash and bonds

Cash and bonds are GREAT investments for the short-run, defined by me as under 5-ish years. I recommend people have any money they need to spend in a year in cash, including any ’emergency funds’ since those could be needed anytime. Bonds, either as a bond fund, or as savings bonds– such as I-bonds— if rates are favorable and you are ok with the extra hassle, are great for the 1 – ~5 year time horizon, or as a percentage of a retirement portfolio once you’re within ~10-15 years of needing to actually live off your investments. Otherwise, keep everything you won’t need for at least 5-15 years in stocks!