You might want to first read my blueprint to early retirement. In order to retire, you need to know how much money to save by the time you plan to exit the rat race.

How do you know how much you need to retire?

Use a calculator

If you know your salary, how much you’re saving per year, your invested assets, and your spending, you can use this calculator.

20x earnings rule of thumb

The simplest, but not the best, way to is to assume you’ll need 20x your annual spending in order to retire indefinitely without any other income beyond your own savings. Divide your non-house net worth (all your retirement + other savings) by the amount you/your family would need to live on once you retired. Factor in extra spending for buying your own health insurance until Medicare kicks in, for kids if you got ’em (don’t forget about college), and anything else you can reasonably foresee.

Let’s say your family spends $72,000 per year ($6,000 per month) currently, and expects that to rise to $80,000 for kid’s expenses as they age + annual college savings, plus another $10,000 for catastrophic health insurance once you quit your job. That’s $90,000 you’ll need each year in retirement. 20x that is $1.8 million. 25x is $2.25 million. This is a good rough estimate, but you also need to consider what sources of income you can tap prior to age 60 and after age 60, including social security and any fixed pensions you’ll receive.

Figuring out before-60 money and after-60 money

To avoid fees & penalties, it’s imperative that you don’t tap your retirement accounts until you’re allowed to do so. In most cases this means waiting until you’re 59.5 to access any money in your 401k or Traditional IRA, and before touching any earnings in your Roth IRA. For your HSA, if you want to use it for non-medical expenses without penalty you must wait until you’re 65.

Roth IRA contribution early withdrawals are ok, though!

If you need to, you can access all of the contributions you’ve made to a Roth IRA over the years at any time without penalty or taxes, so keep good records of how much you’re contributed to any Roth IRA throughout your investing history. If your Roth IRA is worth $100,000 at age 50 and you had contributed $40,000 to it to date, you are allowed to take out up to that $40,000 at any time and for any reason with paying any taxes (since you already paid them when the money went in) or penalties. You could use this $40,000 if needed before age 59.5. When you hit 59.5, you can access the $60,000 in earnings as well without any penalties (or taxes, since it’s a Roth.)

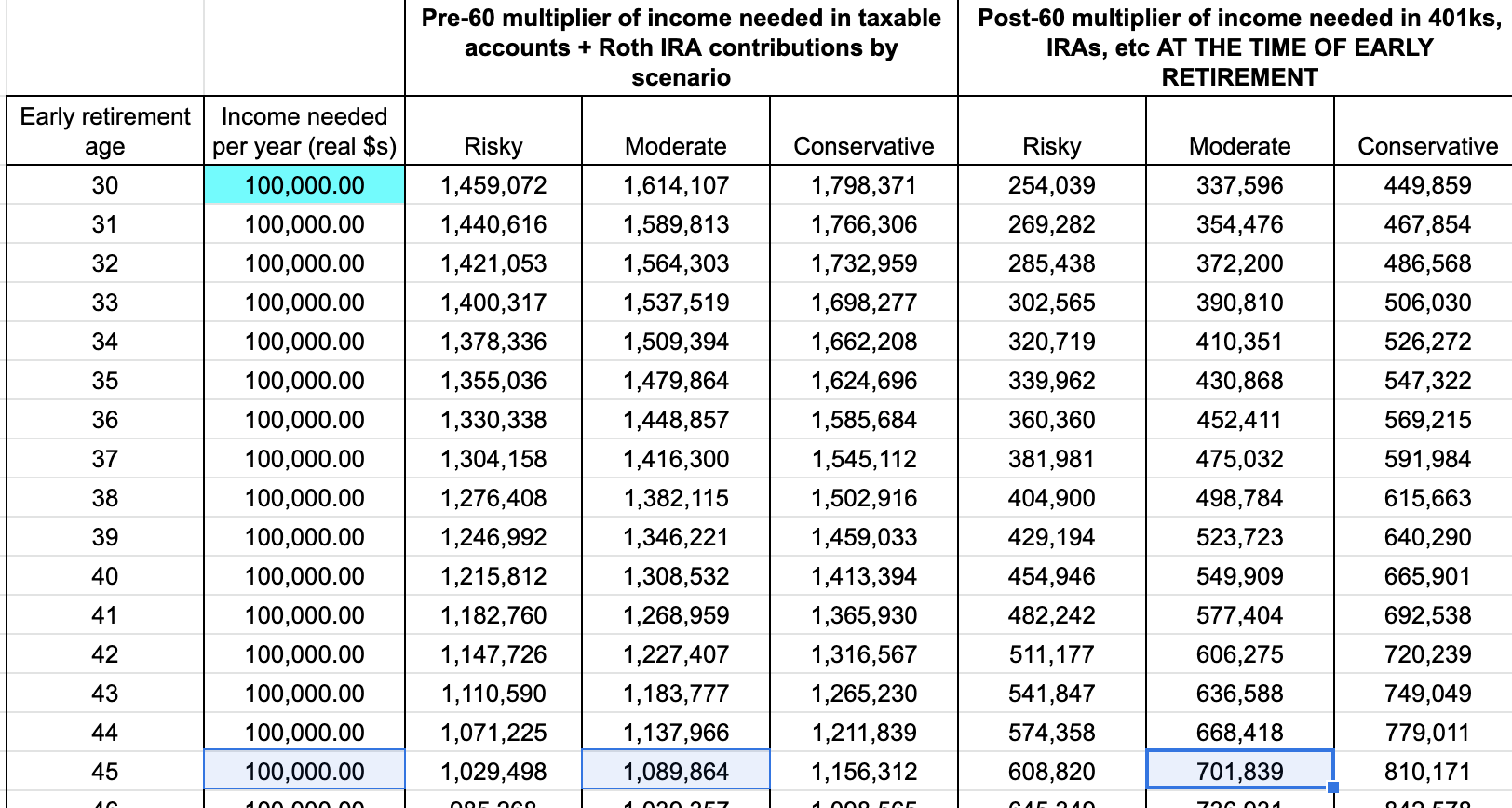

Here’s how much you will need in pre-60 vs post-60 accounts based on your planned retirement age

You’re free to do some custom spreadsheet calculations on your own, or with a spreadsheet-loving friend, to make sure you’re saving roughly the right amounts in your ‘after 60’ accounts (401k/IRA/pension/social security) vs your ‘before 60’ accounts: taxable accounts + HSA for health care out-of-pocket expenses only + Roth IRA contributions.

A simple solution is to use this calculator created by Ian Johnson.

Or if you prefer, my clunkier Google Sheet (see table below) to look up your pre-60 and post-60 savings needs. Match up the age you plan to retire with the two multipliers on the right that tell you how many times your spending you need. (You can also copy this sheet and replace the blue-highlighted ‘1’ with your estimated spending to see it in dollars.)

For example, if you planned to retire at age 45, you’d need 11x your annual income to make it to age 60 under my ‘moderate’ risk scenario*

If you needed $100,000 for your family to live on, you’d need to have $1.1 million (11 * $100 K) at age 45 in taxable accounts + Roth IRA contributions.

The same row above also shows that you’d need 7x your needs in your post-60 sources at age 45 (this money will keep growing and be even more at 60.) So that’s an additional $700,000 you’d need in 401ks and the like. That means you would need a grand total of $1.8 M at age 45 to retire on $100,000 a year using only your savings. (If you planned on social security or a pension or other income in retirement, you’d need less in your post-60 accounts.)

This table can help you calculate when you can retire as well as how you should try to split your money between pre- and post-60 sources.

I personally have never not maxed out a tax-advantaged source in order to put more into a non-retirement source. This is because I’d rather just maximize my total wealth even if it means I’ll have a little more in post-60 retirement vs pre-60. That said, if you were really serious about not working at all in your pre-60 early retirement, you should consider how your wealth will be divided.

* 'Moderate' assumes 5% real market returns on that 11x of annual income from age 45 - 60. Risky assumes 6% real returns, conservative assumes 4%. These roughly correlate to the expected returns after taxes and inflation from a 90-10 stock-to-bond portfolio like the Vanguard Target Retirement fund that I recommend. What you actually experience will depend on the market and your particular tax and investment choices, but it should be close enough.

Now that you know how much you need, how do you know how much you need to save from now until early retirement?

You can use a retirement calculator like the one above to compute how much you’d need to save each year to get to your age target. This will help show you whether you’re on track, or whether you really need to cut spending (and/or make more money) in order to hit your target retirement age.

These numbers are not set in stone

These calculations give you a ballpark feel for what you need, but in reality you’ll need to be flexible. Can you lower your spending if the market takes a dive? Are you willing to go back to work, perhaps only part-time, if you need to? Will your health or any other circumstance require more money than you anticipate, and what can you do to mitigate that (hint: get and stay healthy)?

If you’re willing to work part-time or expect other sources of income like a pension or social security, you can definitely retire with less, but you should do some more spreadsheet math to estimate all this.

Lastly, remember that financial advisors like me tend to give cautious advice when it comes to financial risk. Given that, don’t only consider the risks of retiring too early; consider the risks of retiring too late. Whiling away your life in a passionless malaise in a career you’re not crazy about is a risk to your happiness and life-satisfaction. You might be better off taking more financial risk in exchange for less risk of regret. No one lies on their deathbed wishing they spent more time at the office.

With these estimates and my early retirement blueprint, how you want to live the rest of your life is up to you.

This was a lovely blog ppost